You're About to Retire… Can We Talk About Timing?

Jul 11, 2026

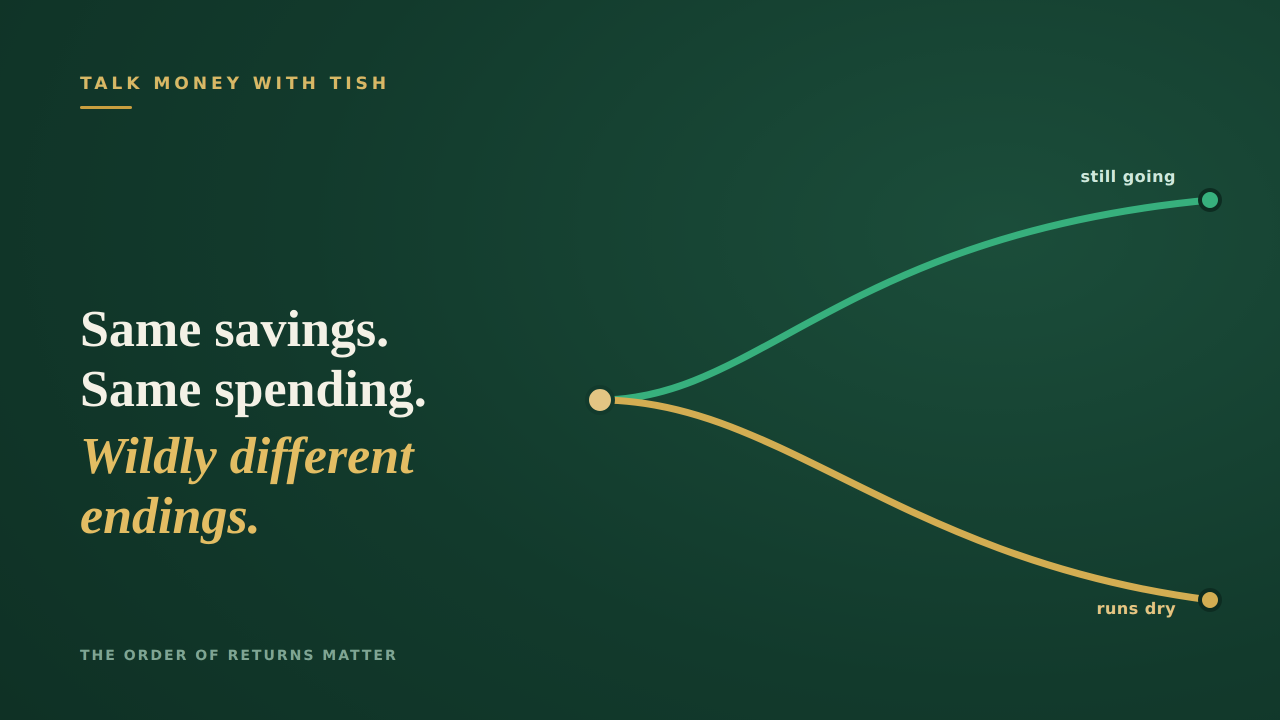

Same savings. Same spending. Wildly different endings.

By Christina Carlisle

Last Tuesday I spent time watching the markets and headlines, and I also had a conversation with someone approaching retirement. What struck me in both wasn't the numbers. It was the fear.

Sound familiar?

Real fear. They said something I haven't been able to stop thinking about:

"I've saved for 40 years. Now I have to make it last the rest of my life — and I only get one shot at it."

That's the sentence that made me sit down and write this.

If you know me, you know I pay close attention to life's transition points — those moments where things shift and the margin for error suddenly feels a lot smaller. Divorce. A career blowup. A health scare. Turning 40 (or 50, or 60) and wondering how you got here. I've lived a few of these myself, and here's what I've learned: they are terrifying and they are opportunities, at the very same time.

Retirement is one of the biggest transitions of all. But unlike the others, we tend to talk about it almost entirely in terms of numbers — how much you have, how much you need, what your "number" is — and not nearly enough in terms of risk.

But there's a piece of this that almost nobody warns you about. And once you see it, you can't un-see it.

The Thing Nobody Warns You About

Here's what most people believe: as long as my investments earn a decent average return over my retirement, I'll be fine.

It sounds reasonable. It's also not the whole story. Because whether your money actually lasts doesn't just depend on the average return you earn. It depends on the order those returns show up in — especially in the first handful of years after you stop working.

The financial world has a name for this. It's called sequence-of-returns risk. Clunky term, I know. But the idea underneath it might be the most important thing you were never taught about retirement, so stay with me — I'll make it simple.

Picture two people. Same nest egg. Same yearly spending. Same 30-year retirement. And here's the kicker: over those 30 years, they earn the exact same average return. Identical.

And yet one of them dies with money to spare… while the other runs out, with years still ahead of them.

How is that even possible?

Timing. Pure timing.

The one who runs out had the bad luck of retiring right before a rough stretch in the market. So in those very first years — when their savings were at their biggest, and they'd only just started drawing on them — they were selling investments while they were down just to pay the bills. And every withdrawal in a down market is like pulling bricks out of the foundation. When the market finally recovered, there was simply less money left to recover with. The comeback happened. They just weren't fully invited to it.

The other one? They got their good years first. Their early retirement rode a rising market, their savings actually grew even as they spent them, and by the time a rough patch eventually rolled around, they'd built such a cushion that it barely touched them.

Same average return. Wildly different endings. The only real difference was when the storm hit.

That's sequence-of-returns risk in a nutshell. And here's the part that should get your attention: you don't get to pick when you're ready to retire, and you certainly don't get to pick what the market does that year. Which means whether your money lasts or runs dry is, to a genuinely scary degree… luck.

Three People, Three Very Different Stories

Let me make this even more real. Think about three people, retiring at three different moments.

The one who retired about 10 years ago basically won the lottery — and probably doesn't even know it. They walked straight into a long, strong stretch of market growth. Even the sharp scare of 2020 bounced back almost before anyone could finish panicking. Their money grew while they spent it. Today they feel secure and maybe even a little clever, and a scary headline barely makes them blink. Here's the uncomfortable truth, though: most of that wasn't brilliance. It was timing.

The one retiring right now is walking a very different road. They're stepping in near the top of a long run-up, into a market that suddenly feels jittery — nervous headlines about oil prices and interest rates, the whole world feeling a little on edge. This is the person I worry about most. Because if a rough patch shows up in these first few years, it does the most damage of all. This is the danger zone.

And the one retiring a year or two from now? Honestly — nobody knows. It could be calmer. It could be worse. And that uncertainty is exactly the point.

See the thread running through all three? The timing is mostly luck. And I don't know about you, but I refuse to hand my future over to luck and just hope it decides to be kind to me.

So let's talk about what you actually can control.

The Part You Actually Get to Control

This is where my "mindset" side and my "money" side finally shake hands. Because the goal was never to control the weather. The goal is to prepare well enough that the weather doesn't get to decide your whole future for you.

There's some really good research from EY on exactly this, and it comes down to two beautifully simple ideas.

Idea #1: Build yourself a buffer to spend from in the bad years.

Think of this as a separate pool of money that lives outside your investment accounts — something like cash value life insurance is one example of where it can come from. Its entire job is to give you somewhere else to reach for when the market is down.

And here's why that's so powerful. Remember the real problem in that first story? Our unlucky retiree was a forced seller — no choice but to cash out investments while they were low, just to pay the bills. A buffer erases that problem. In a down year, you spend from the buffer instead. You let the market do its ugly thing, you leave your investments alone, and you give them the time and space to climb back. You stop yanking bricks out of the foundation at the worst possible moment. That's it. That's the magic.

Idea #2: Give yourself a paycheck that never stops.

This one is about turning a slice of your savings into guaranteed income for life — the kind of thing certain annuities, like a fixed indexed annuity, are built to do. You commit a portion up front, the rest of your money stays invested and working, and in return you get a check that keeps showing up for the rest of your life. No matter what the market does. No matter how long you live.

And here's the emotional part, which matters more than people like to admit: when you know your basic bills are covered by income that literally cannot run out, a scary market stops feeling like a threat to your survival. Your groceries aren't riding on this month's headlines. You're never forced to sell in a panic just to get by. That peace of mind is its own kind of return.

Now, let me be straight with you: neither of these is free. Protecting yourself usually costs a little bit of your upside. In a roaring market, the person who took no protection and just let it all ride might well end up richer — and I won't pretend otherwise. But that same unprotected person is also the one most likely to run out of money if the timing turns against them.

So the real question isn't "How do I squeeze out the absolute most?" It's "How do I make sure I'm okay — even if the timing isn't?"

So Here's Something to Actually Do With This

I'm not going to hand you a big, scary idea and then just leave you standing there holding it. That's not my style, and you know it. A risk you understand but never actually do anything about doesn't keep you safe. It just keeps you up at 2 a.m.

See it for yourself

Watch what timing does to a retirement — in real time

I built a simple, interactive tool. Plug in a nest egg and what you'd like to spend each year, then flip a switch to see what happens when the bad years hit early instead of late. Turn the two protections on and off and watch whether the money lasts — or runs out.

Try the interactive tool →Go play with it. Move the sliders. Break it. Scare yourself a little… and then reassure yourself a lot.

Because here's what I've learned, over and over, in every transition I've walked through:

Fear shrinks the moment you stop staring at the unknown and start preparing for it.

The market will do what the market does. Your job isn't to outguess it — it's to make sure it can't wreck you.

If you're staring down retirement right now, wondering whether your plan could survive a rough first few years, that's not a fear to bury. It's a conversation to have. And I'm always up for it.

Disclaimer: This is for educational purposes and not advice. Before you move a single dollar, you should speak with a trusted licensed professional who understands your whole financial picture.

Source & further reading: EY, "The benefits of integrating insurance products into a retirement plan."